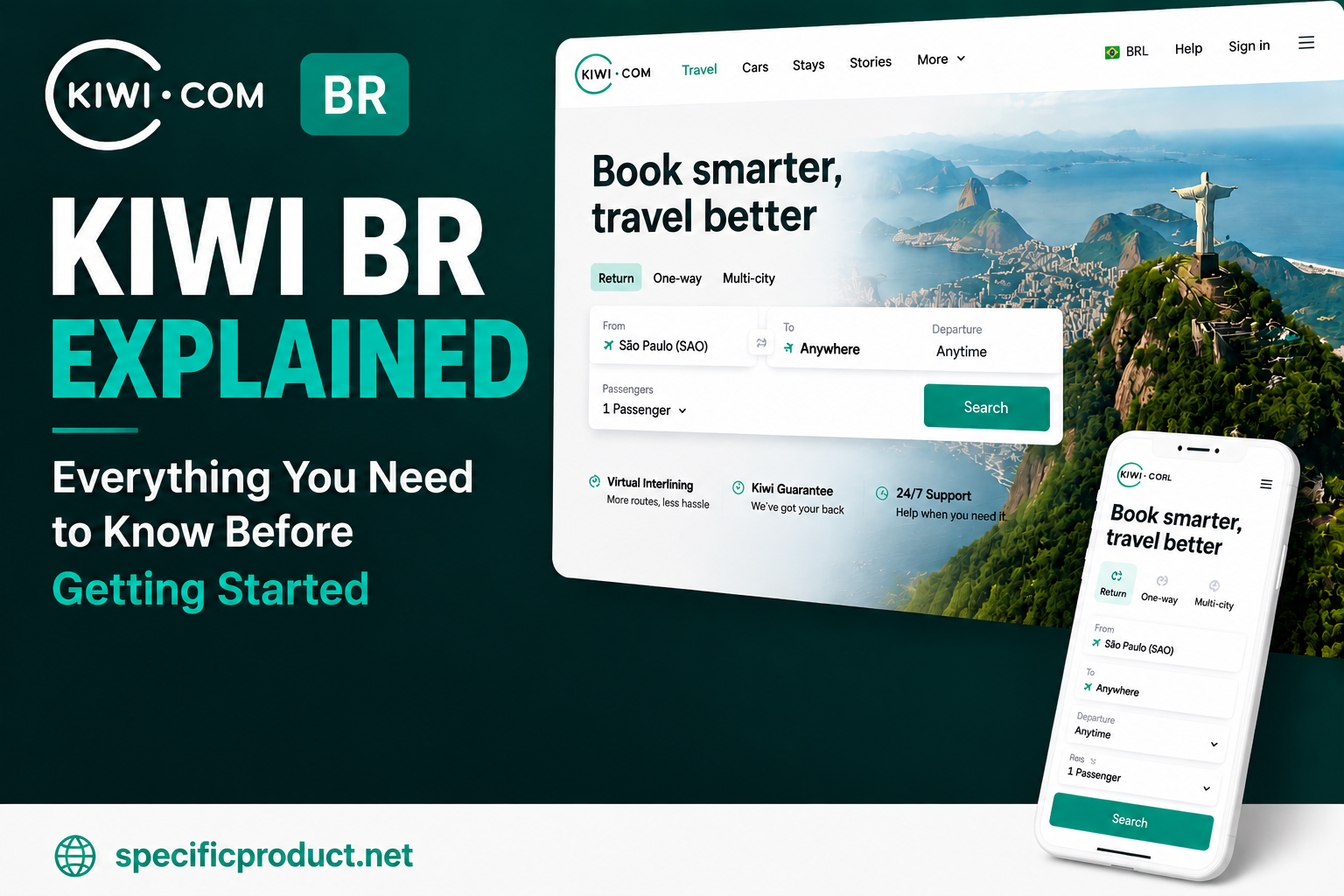

Kiwi BR Explained: Everything You Need to Know Before Getting Started

The world of digital payments is changing faster than ever, especially in countries like India where Unified Payments Interface (UPI) has become a household name. But what if you could tap into credit, not just debit, through that same familiar UPI system? That’s where Kiwi BR comes in — a fintech solution combining credit card features with everyday digital payments. In this deep‑dive guide, we’ll break down everything you need to know before diving in. From how it works to why it’s gaining attention, by the end you’ll fully understand Kiwi BR and how it might fit into your financial life.

Table of Contents

- 1 What Is Kiwi BR?

- 2 The Problem Kiwi BR Aims to Solve

- 3 How Kiwi BR Works (Credit on UPI)

- 4 The Kiwi Onboarding Process

- 5 Kiwi BR Benefits You Should Know

- 6 Features and Functionalities of Kiwi BR

- 7 Potential Risks and Considerations

- 8 Kiwi’s Product Offerings

- 9 Kiwi’s Growth and Funding Journey

- 10 Important Considerations Before Joining

- 11 Real‑World User Experiences

- 12 Who Should Use Kiwi?

- 13 Tips to Maximize Rewards

- 14 Future Roadmap of Kiwi BR

- 15 Why Users Are Excited About Kiwi BR

- 16 Real‑World Use Cases of Kiwi BR

- 17 Tips for Getting the Most Out of Kiwi BR

- 18 Conclusion

- 19 Frequently Asked Questions

What Is Kiwi BR?

At its core, Kiwi BR refers to the Kiwi fintech platform focused on offering credit solutions through UPI and RuPay credit cards. Launched in 2022 by seasoned fintech veterans, Kiwi is pioneering what’s known as “Credit on UPI” in India — meaning users can leverage credit card power directly through the UPI interface that billions already use daily.

While the name “Kiwi BR” is often used informally by users and in discussions online, it’s important to understand it as part of the broader Kiwi ecosystem — especially a service designed to bring convenient credit access to a larger audience.

The Problem Kiwi BR Aims to Solve

Traditional credit access has long been a bottleneck for many users. Banks often take time and strict underwriting processes to approve credit cards. That leaves millions of people digitally active but without easy credit access.

Enter Kiwi BR — built around the idea that digital convenience should also include credit convenience. By fusing credit issuance with UPI’s already massive user base, Kiwi helps bridge that gap. Rather than waiting days for a card approval, Kiwi aims to make credit available quickly and seamlessly.

How Kiwi BR Works (Credit on UPI)

So how does Kiwi actually function? The key lies in Credit on UPI — an innovation made possible by regulatory changes that allow RuPay credit cards to be linked directly to UPI IDs. Traditionally, UPI was tied to bank accounts or debit cards only. Now, Kiwi issues virtual RuPay credit cards, which users can link to UPI and use just like a credit facility.

This means you can make payments at any UPI‑enabled merchant, both online and in physical stores, using credit without needing a physical plastic card in your pocket. It’s like giving your smartphone an invisible credit card that works everywhere UPI does.

The Kiwi Onboarding Process

Getting started with Kiwi BR usually follows a few simple steps:

- Download and Install the App: Available on major app platforms.

- Complete KYC: Identity verification via video and biometrics.

- Receive Your Virtual Credit Card: Instant or near‑instant issuance.

- Link to UPI: Connect it with your UPI ID for payments.

- Start Using: Pay with UPI but enjoy credit features.

What sets Kiwi apart is the simplicity. No paperwork, no waiting in bank queues — everything is mobile‑first and fast.

Kiwi BR Benefits You Should Know

Easy Access to Credit

For many, getting a traditional credit card is a lengthy and sometimes frustrating process. Kiwi offers a faster, digitally native alternative that still gives the core credit card experience.

Cashback Rewards

Kiwi’s reward program ensures you’re not just paying — you’re also earning back a portion of what you spend. This makes everyday transactions more rewarding than with a standard UPI payment alone.

Seamless Integration With UPI

UPI is already ubiquitous across India — millions use it daily for everything from grocery bills to travel tickets. Kiwi taps directly into that ecosystem, making credit adoption as easy as a few taps on your phone.

Features and Functionalities of Kiwi BR

Virtual RuPay Credit Card

One of the standout features of Kiwi is the virtual RuPay credit card. Issued in partnership with banks such as AU Small Finance Bank and Yes Bank, this card becomes the backbone of your Kiwi experience. Once issued, it’s automatically linked to your UPI ID and ready to use for payments.

Cashback Rewards System

Unlike many standard UPI payments where you earn nothing, Kiwi users can earn cashback rewards on transactions. This isn’t tied just to the UPI app — it’s connected to the credit card experience, meaning QR code payments can earn you real money back in your bank account.

Instant Approvals and Convenience

Kiwi is designed for speed and ease. The founders built the platform with quick onboarding in mind, leveraging video KYC and biometric authentication to cut down waiting times drastically compared to traditional cards.

Optional Membership Perks

Some Kiwi plans offer additional benefits — like higher cashback tiers or premium perks — through optional memberships. These are typically paid annually and designed for users seeking more value out of their Kiwi experience.

Potential Risks and Considerations

Of course, credit comes with responsibility. Users must be mindful of overspending and ensure they repay on time to avoid interest or financial stress. And while Kiwi brings innovation, it also competes in a rapidly evolving fintech space with players like OneCard, Slice, and others vying for attention.

Kiwi’s Product Offerings

Kiwi’s core product is its virtual RuPay credit card, but there are a few related offerings worth knowing:

- Virtual Credit Cards: Issued digitally, usable through UPI.

- Neon Membership: A paid annual plan (around ₹999) that unlocks higher cashback tiers and additional perks on spends.

- EMI Features: Kiwi has also introduced interest‑backed EMI options on UPI with cashback, letting users split big purchases into instalments with attractive rewards.

These product variants give users flexibility depending on how they want to use credit and maximize rewards.

Kiwi’s Growth and Funding Journey

Kiwi’s trajectory has been notable. Starting with seed funding, it raised millions to fuel its vision — including Series A rounds and a substantial $24 million Series B led by Vertex Ventures to expand its Credit‑on‑UPI offerings.

These investments underscore confidence in Kiwi’s model and the potential of credit on real‑time payment rails like UPI.

Important Considerations Before Joining

Before creating a Kiwi account, there are a few things you should consider:

- Eligibility & CIBIL: Kiwi typically evaluates your creditworthiness before issuing credit. Without a minimum CIBIL score or credit history, approval may be harder.

- Transaction Minimums: Some cashback rewards require minimum transaction values (e.g., ₹100 or more on UPI).

- Merchant Acceptance: Not all merchants accept credit‑on‑UPI yet, which could limit usefulness in some cases.

User discussions also highlight that Kiwi’s customer service might not be as responsive as traditional banks’, so patience (or backups) can help.

Real‑World User Experiences

Actual Kiwi users share a mix of feedback:

- Positive Insights: Many report smooth UPI payments, consistent cashback, and a largely functional app experience.

- Challenges: Opinions vary — some users experience delays in support, blocked accounts during signup, or confusion about offers that aren’t active yet.

These real‑world voices highlight the importance of setting expectations: Kiwi can offer great rewards and convenience, but it may not be flawless.

Who Should Use Kiwi?

Not every financial product is for everyone. But Kiwi has carved out a niche:

- Young professionals who are new to credit.

- First‑time credit card users who prefer digital experiences.

- Frequent UPI users who want rewards on everyday spends.

- People looking to build or improve their credit profile.

Kiwi isn’t just for heavy spenders — in fact, many users find its rewards most beneficial on small, frequent transactions like food, rides, or groceries.

Tips to Maximize Rewards

To get the most out of Kiwi:

- Use UPI payments over traditional credit card swipe when possible.

- Meet the minimum transactions and cashback criteria.

- Consider the Neon membership if you transact heavily and want higher rewards.

Always cross‑check the latest terms in the app, as offers can change.

Future Roadmap of Kiwi BR

Looking ahead, Kiwi plans to deepen partnerships with major banks and expand credit features. The goal is ambitious: issue millions of RuPay credit cards linked to UPI, allowing more users to enjoy credit seamlessly.

This could transform how digital credit is accessed — making Kiwi a central hub for UPI‑based credit services.

Why Users Are Excited About Kiwi BR

From everyday shopping to big‑ticket purchases, Kiwi’s blend of convenience, rewards, and accessibility is appealing — especially for digital‑native users who want credit without complexity. With UPI already deeply embedded in daily life, this credit layer feels like the next logical step.

Real‑World Use Cases of Kiwi BR

Whether buying groceries, dining out, or booking travel, Kiwi’s credit‑enabled UPI payments unlock flexibility. Even high‑value purchases like electronics or appliances can be broken into manageable credit transactions with rewards attached — something traditional UPI alone can’t offer.

Tips for Getting the Most Out of Kiwi BR

To maximize value:

- Use cashback wisely: Choose transactions where cashback is highest.

- Pay promptly: Avoid interest and maintain strong credit health.

- Monitor usage: Track through the app for insights.

These habits ensure you enjoy Kiwi’s perks without pitfalls.

Conclusion

Kiwi BR represents a bold leap in digital finance by blending the convenience of UPI with the power of credit. For users seeking quick access to credit, reward‑driven transactions, and a seamless mobile experience, it’s a strong option worth exploring. As it expands and innovates, Kiwi could very well redefine how millions manage credit in a digital‑first world.

Frequently Asked Questions

Q. What exactly is Kiwi BR?

Kiwi BR refers to the Kiwi fintech service that offers credit on UPI by issuing virtual RuPay credit cards.

Q. Can anyone use Kiwi BR?

Eligibility often depends on basic KYC and credit validation, similar to most credit services.

Q. Is Kiwi BR free?

The basic service typically has no annual fees, though optional premium tiers may charge.

Q. How do I earn cashback with Kiwi BR?

Cashback is earned through qualifying UPI payments linked to your Kiwi‑issued credit card.

Q. Is the Kiwi credit secure?

Kiwi partners with regulated banks and uses secure UPI and card networks, making it safe for transactions.

Recent Post

How BathMate Works: A Complete Beginner’s Guide

Fidelcrest Investment: A Complete Guide to Prop Trading Opportunities

Top Benefits of Using BlackBull Markets Banking/Trading Services

How The Escape Game Entertainment Creates Unforgettable Group Adventures

Why the Invoxia Affiliate Program Is a Smart Choice for Tech Bloggers

Why the Proton Partners Program Is Gaining Popularity Among Affiliates

How xTool Helps Entrepreneurs Start a Profitable Custom Product Business

Atlas VPN Review: Features, Security, Pricing, and Performance Explained

The Complete Uncrate Guide for Men Seeking Quality Gear and Inspiration

Releted Post